csi csc2 practice test

Canadian Securities Course Exam 2

Question 1

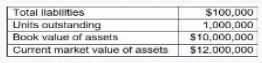

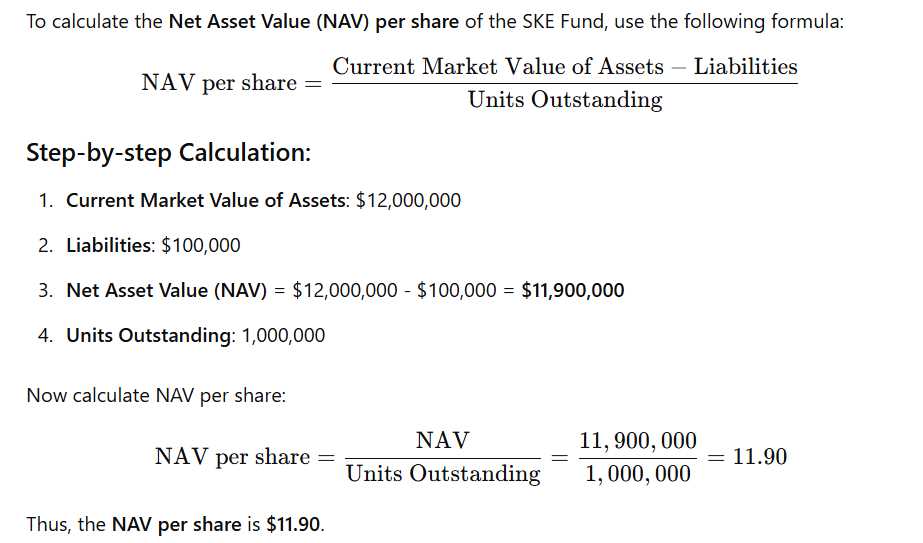

The following financial information is available for fund SKE:

What is SKE fund’s net asset value per share?

- A. $9,90

- B. $11, 90

- C. $12,00

- D. $10, 00

Answer:

B

Explanation:

Explanation of Answer Options:

Option A ($9.90): Incorrect; this value does not reflect the subtraction of liabilities.

Option B ($11.90): Correct; it accounts for the subtraction of liabilities and proper division by

outstanding units.

Option C ($12.00): Incorrect; it represents the market value of assets per unit without deducting

liabilities.

Option D ($10.00): Incorrect; this value does not align with the given data or calculations.

Reference to Canadian Securities Course Exam 2 Study Materials:

Volume 2, Chapter 17 - Mutual Funds: Structure and Regulation, Pricing Mutual Fund Units:

Discusses the formula for calculating NAV per share, including the treatment of liabilities and market

value of assets.

Volume 2, Chapter 22 - Other Managed Products:

Covers the concept of valuation for managed funds and its importance for accurate pricing.

Volume 1, Chapter 11 - Corporations and Their Financial Statements:

Provides foundational knowledge about book and market values used in calculations.

Question 2

How are investment dealers unique participants in the institutional market?

- A. They manage pools of assets on behalf of beneficiaries.

- B. They act on both they buy side and sell side.

- C. They produce research reports.

- D. They manage a firm’s financial assets in support of a company’s business activities.

Answer:

B

Explanation:

Investment dealers play a unique role in the institutional market due to their dual capability of

operating on both the buy side and the sell side:

The Buy Side

Investment dealers assist institutional investors like pension funds, mutual funds, and hedge funds in

acquiring securities to meet their investment objectives. These clients aim to optimize returns on

their invested assets, and the dealers provide them with access to securities markets, investment

advice, and execution services.

The Sell Side

On the sell side, investment dealers facilitate the issuance of new securities. They underwrite and

distribute these securities, providing liquidity to the market. They also produce research reports and

provide trade execution services to institutional and retail clients. This dual operation is critical for

maintaining market efficiency and ensuring the smooth functioning of capital markets.

This dual-role capacity makes investment dealers pivotal in bridging gaps between the needs of

securities issuers and institutional investors. They enhance market liquidity, efficiency, and

transparency through their intermediary functions.

Reference:

Canadian Securities Course, Volume 1, Chapter 1: The Investment Dealer’s Role as a Financial

Intermediary

Canadian Securities Course, Volume 2, Chapter 27: Working with the Institutional Client.

Question 3

Tom sold some bonds in his RRSP and used the total $100,000 in proceeds to buy a 75% guaranteed

segregated fund. Three years later, Tom died. At the time of his death, the market value of the

segregated fund was $700,000. Assuming no interim withdrawal on market value reset, what is the

death benefit payable from this investment?

- A. $0,

- B. $70,000

- C. $30,000

- D. $5, 000

Answer:

C

Explanation:

Key Concepts:

A segregated fund with a guaranteed death benefit ensures that the investor (or their estate)

receives at least a certain percentage of the initial investment in case of death. This percentage is

applied to the original investment amount, and if the market value of the segregated fund at the

time of death is lower than this guaranteed amount, the insurance company pays the shortfall.

Step-by-step Explanation:

Initial Investment in the Segregated Fund:

Tom invested $100,000 into a segregated fund with a 75% death benefit guarantee.

Guaranteed amount = 75% × $100,000 = $75,000.

Market Value at the Time of Death:

The market value of the segregated fund is $70,000 at the time of Tom's death.

Shortfall Calculation:

The guaranteed amount ($75,000) is greater than the market value ($70,000).

Shortfall = $75,000 - $70,000 = $5,000.

Death Benefit Payable:

Since the segregated fund guarantees at least $75,000, the insurance company will pay the shortfall

of $5,000 to the estate.

Answer:

Option A ($0): Incorrect; there is a shortfall between the guaranteed amount and the market value,

so a payout will occur.

Option B ($70,000): Incorrect; this is the market value, not the shortfall amount.

Option C ($30,000): Incorrect; this value does not align with the 75% guarantee calculation.

Option D ($5,000): Correct; this is the shortfall amount payable as the death benefit.

Reference to Canadian Securities Course Exam 2 Study Materials:

Volume 2, Chapter 22 – Segregated Funds

Explains death benefit guarantees in segregated funds and how the shortfall is calculated.

Volume 2, Chapter 24 – Canadian Taxation

Highlights how RRSP investments, such as segregated funds, are treated upon the investor's death.

Volume 2, Chapter 26 – Working with the Retail Client

Discusses estate planning considerations, including the role of segregated funds in ensuring financial

protection.

Question 4

In Canada, which industries are categorized as defensive?

- A. Baking and materials

- B. Energy and materials.

- C. Energy and utilities.

- D. Banking and utilities.

Answer:

D

Explanation:

Defensive industries are less sensitive to economic cycles. They tend to perform consistently

regardless of economic conditions because they provide essential goods and services that consumers

require regardless of their financial situation. Banking and utilities fall under this category as:

Banking ensures essential financial services.

Utilities (e.g., electricity, water) provide necessary services.

Industries like energy and materials are more cyclical, reacting strongly to economic fluctuations.

Hence, D. Banking and Utilities is the correct choice.

Reference:

Volume 2, Chapter 13, "Classifying Industries by Reaction to the Economic Cycle".

Question 5

Which type of market participant is generally regulated as an alternative trading system?

- A. Venture exchange

- B. Pink sheets

- C. Dark pool

- D. Over-the-counter bulletin board.

Answer:

C

Explanation:

An alternative trading system (ATS) is a trading platform that is not a formal stock exchange but

allows for the buying and selling of securities. A dark pool is a type of ATS where trade details are not

displayed until after execution, providing anonymity to large institutional trades. Other options like

venture exchanges, pink sheets, and OTC bulletin boards are not considered ATSs.

Reference:

Volume 1, Chapter 9, "Alternative Trading Systems".

Question 6

In March of this year, a client buys 1,000 PIL inc, common shares at $16 per share and pays a

commission of $25 on the purchase. Several months later in the same year, the client sell the shares

at $12 per share and pays commission of $50 on the sale. What is the client’s allowable capital loss

on the transaction?

- A. $2,038

- B. $2,025

- C. $1,925 D.$2,013

Answer:

A

Explanation:

To calculate the allowable capital loss, we must first determine the adjusted cost base (ACB) and the

proceeds of disposition (POD), then subtract the latter from the former. Commissions on both the

purchase and sale are included in the calculation.

Step-by-Step Explanation:

Purchase Details:

Number of shares purchased: 1,000

Purchase price per share: $16

Total purchase cost before commission: $16 × 1,000 = $16,000

Add purchase commission: $25

Adjusted cost base (ACB): $16,000 + $25 = $16,025

Sale Details:

Number of shares sold: 1,000

Sale price per share: $12

Total sale proceeds before commission: $12 × 1,000 = $12,000

Deduct sale commission: $50

Proceeds of Disposition (POD): $12,000 - $50 = $11,950

Capital Loss Calculation:

Capital loss = ACB - POD

Capital loss = $16,025 - $11,950 = $4,075

Allowable Capital Loss:

In Canada, 50% of the capital loss is allowable for tax purposes.

Allowable capital loss = 50% × $4,075 = $2,038

Final Answer:

Option A ($2,038): Correct.

Option B ($2,025): Incorrect; likely excludes commissions or contains a minor calculation error.

Option C ($1,925): Incorrect; this does not account for the full adjusted cost base or allowable

percentage.

Option D ($2,013): Incorrect; this likely contains a rounding error or miscalculation.

Reference to Canadian Securities Course Exam 2 Study Materials:

Volume 2, Chapter 24 – Canadian Taxation

Discusses the calculation of adjusted cost base (ACB), proceeds of disposition (POD), and allowable

capital losses.

Volume 1, Chapter 11 – Corporations and Their Financial Statements

Details financial concepts like capital gains, losses, and the treatment of commissions in securities

transactions.

Volume 2, Chapter 26 – Working with the Retail Client

Covers tax implications and planning for securities transactions.

Question 7

Which asset type is classified as a fixed-income asset for portfolio management purposes?

- A. Money market securities

- B. Preferred shares.

- C. Convertible bonds.

- D. Bonds with a maturity of one year or less.

Answer:

C

Explanation:

Fixed-income assets are characterized by predictable cash flows. Convertible bonds qualify because

they have features of fixed-income securities (coupon payments and principal repayment) while also

offering the option to convert into equity.

Money market securities (Option A) are short-term, high-liquidity instruments and typically not

classified as fixed-income for long-term portfolio management purposes.

Preferred shares (Option B) are equity-like instruments with fixed dividend payments but lack the

"fixed-income" designation for portfolio management.

Bonds with less than one year to maturity (Option D) fall under money market classifications rather

than fixed income.

Reference: Canadian Securities Course Volume 2, Fixed-Income Securities Section.

Question 8

What is one advantage of implementing indexing investing style?

- A. Provides preferential tax treatment to distributions in the form of derive-based income.

- B. Simple for investors to understand.

- C. Offers opportunity to outperform the market at a low cost.

- D. Suitable for short-term investing.

Answer:

B

Explanation:

Indexing is an investment strategy that tracks a benchmark index and is simple for investors to

understand. This ease of understanding is one of its primary advantages.

Option A: Indexing does not provide preferential tax treatment for derivative-based income.

Option C: While low-cost, indexing does not offer an opportunity to outperform the market—it aims

to match the market's performance.

Option D: Indexing is typically suited for long-term investing due to its emphasis on broad market

exposure and passive management.

Reference: Canadian Securities Course Volume 2, Portfolio Management Section.

Question 9

Which type of mutual funds tend to have the lowest management fees?

- A. Asset allocation

- B. Small cap

- C. Bond

- D. Index

Answer:

D

Explanation:

Index mutual funds are structured to replicate the performance of a market index, such as the

S&P/TSX Composite Index. Since these funds do not require active management, their management

fees are among the lowest compared to other types of mutual funds. Active management in asset

allocation, small-cap, or bond funds involves more frequent trading and research, increasing

operational costs.

Reference:

CSC Volume 2, Chapter 18: "Mutual Funds: Types and Features," discusses indexing as a fund

management style and highlights its low costs compared to actively managed funds.

Question 10

What type of investment typically involves massive amounts of capital provided by a small number

of investors?

- A. Derivatives

- B. Infrastructure

- C. Bonds

- D. Commodities

Answer:

B

Explanation:

Infrastructure investments often require massive capital commitments for projects such as airports,

highways, and utilities. These investments are typically made by institutional investors or private

equity funds, involving relatively few but large-scale investors due to the high entry cost and the

long-term nature of these investments.

Reference:

CSC Volume 2, Chapter 20: "Alternative Investments: Benefits, Risks, and Structure," explains the

characteristics of infrastructure as an asset class and its association with significant capital

requirements.

Question 11

What must happen for a redemption to be processed from a mutual fund?

- A. Payment for redeemed securities must be within two business days after the NAVPS is determined.

- B. Mutual funds representatives must submit the order within two business days of when the order is received from the client.

- C. The offering price of the mutual fund must be calculated.

- D. The client redeeming the mutual fund must receive a Fund facts document.

Answer:

A

Explanation:

When a mutual fund redemption is processed, the fund must calculate the Net Asset Value per Share

(NAVPS) to determine the redemption price. The Canadian Securities Administrators (CSA)

regulations mandate that payment for redeemed securities be made within two business days

following the calculation of NAVPS, ensuring prompt transactions while protecting investor interests.

Reference:

CSC Volume 2, Chapter 17: "Mutual Funds: Structure and Regulation," details the process and timing

for mutual fund redemptions, including regulatory requirements.

Question 12

What is the key objective for investors in alternative strategy funds?

- A. To match the performance of a reference index.

- B. To maximize risk-adjusted returns.

- C. To achieve absolute returns

- D. To exceed the current rate of inflation.

Answer:

C

Explanation:

Alternative strategy funds aim to achieve absolute returns, focusing on positive returns under

various market conditions rather than comparing performance to a benchmark index. These

strategies often include hedge funds and alternative mutual funds, using techniques like leverage,

short selling, and derivatives to manage risk and enhance returns. The goal is not necessarily to

outperform an index (as in option A) or match inflation rates (option D) but to deliver consistent

positive returns.

Reference

CSC Volume 2, Chapter 21: Alternative Investments: Strategies and Performance, p. 21-3 to 21-24.

Question 13

Which ratio gauges a company’s ability to repay its debts using funds generated from operating

activities?

- A. Cash flow-to-total debt

- B. Interest coverage.

- C. Asset coverage.

- D. Debt-to-equity

Answer:

A

Explanation:

The cash flow-to-total debt ratio assesses a company's ability to repay its debts using cash generated

from its operating activities. It is calculated by dividing operating cash flow by total debt. A higher

ratio indicates better capacity to cover debts. This metric is crucial for evaluating financial health and

understanding a firm's liquidity position. Other ratios listed have different focuses:

Interest coverage (B) measures a company’s ability to pay interest with operating income.

Asset coverage (C) measures the protection provided to creditors.

Debt-to-equity (D) evaluates capital structure but not immediate debt repayment ability.

Reference

CSC Volume 2, Chapter 14: Company Analysis - Risk Analysis Ratios, p. 14-12 to 14-16.

Question 14

Who generally executes portfolio strategy within a buy-side firm?

- A. Portfolio manager.

- B. Head of fixed income

- C. Investment advisor.

- D. Trader

Answer:

A

Explanation:

Within a buy-side firm, the portfolio manager is responsible for executing the portfolio strategy. They

oversee investment decisions, asset allocation, and security selection based on the investment

mandate and client objectives. Other roles:

Head of fixed income (B) specializes in fixed-income securities rather than overall strategy.

Investment advisor (C) interacts with clients, focusing on advice rather than execution.

Trader (D) carries out transactions but does not set the portfolio strategy.

Reference

CSC Volume 2, Chapter 27: Working with the Institutional Client - The Buy-Side Portfolio Manager, p.

27-8.

Question 15

Which type of commodity ETF is most suitable for an investor seeking to gain exposure to the spot

price of a commodity?

- A. Physical-based

- B. Swap-based

- C. Futures-based.

- D. Equity-based

Answer:

A

Explanation:

Commodity Exchange-Traded Funds (ETFs) provide investors with exposure to commodities such as

gold, oil, and agricultural products. The most suitable type of commodity ETF for gaining exposure to

the spot price of a commodity is the Physical-based ETF because it involves direct ownership or

storage of the commodity. For instance, gold ETFs backed by physical gold store bullion in vaults.

1. Physical-based ETFs

These ETFs hold the actual commodity in physical form, which ensures a close tracking of the spot

price. Physical gold ETFs, for example, store gold bars and adjust the NAV (Net Asset Value) based on

the current spot price. This eliminates discrepancies caused by futures contracts or swaps, making

them ideal for tracking spot prices.

2. Swap-based ETFs

These rely on derivative agreements (swaps) to replicate the price movements of a commodity.

While cost-effective, they do not hold the actual commodity, and their performance may slightly

deviate from the spot price due to tracking errors or counterparty risks.

3. Futures-based ETFs

These use futures contracts to gain exposure. However, futures contracts come with complexities

such as contango and backwardation, which can cause performance differences from the spot price

over time.

4. Equity-based ETFs

These invest in shares of companies involved in the commodity sector (e.g., mining or energy

companies). Their performance is influenced by company-specific factors and broader equity market

trends, making them unsuitable for tracking spot prices.

Reference from CSC Study Documents:

Exchange-Traded Funds, Chapter 19, Volume 2: Discusses the characteristics and structure of ETFs,

including commodity-based ETFs and their classification.

Risks related to tracking error and direct ownership of assets are highlighted under ETF types in

Section 19.