Acams cams-fci practice test

Advanced CAMS-Financial Crimes Investigations

Question 1

The investigative department of a financial institution (Fl) receives an internal escalation notice from

the remittance department for a SWIFT message requesting a refund due to potential fraud. The

notice indicates that a total of three international incoming remittances were transferred to a

corporate customer from Country A, in the amount of approximately 5 million EUR for each. The first

two incoming remittances had been exchanged into currency B and transferred out to Country B a

few days ago. The third incoming remittance has been held by the remittance department.

As noted from the KYC profile, the corporate customer is working in the wood industry. with the last

account review completed 3 months ago. Since the account's opening. there has been no history of a

large amount of funds flowing through the account. The investigator conducts an Internet search and

finds that the remitter is a food beverage company.

The same morning, the investigator receives a call from a financial intelligence unit (FIU) inquiring

about the same incident. The FIU states that it will issue a warrant to freeze the account on the same

day.

After further review, the decision is made that transactions appear suspicious. Which are the next

steps the investigator should take? (Select Two.)

- A. Close the customer's accounts since the FIU is issuing a warrant to freeze the funds.

- B. Contact local LE and advise them of the investigation details to help speed up the investigation and prosecution.

- C. Provide additional information to the LE upon receiving a formal request.

- D. Close the investigation as the FIU is already on this matter, and they will inform LE if needed.

- E. Gather all the information that would be useful for law enforcement (LE) and recommend filing a SAR/STR

Answer:

C, E

Explanation:

The correct answer is C and E. The investigator should provide additional information to the LE upon

receiving a formal request, and gather all the information that would be useful for LE and

recommend filing a SAR/STR. These steps are consistent with the best practices of conducting

financial crime investigations and reporting suspicious activity. The investigator should not close the

customer’s accounts or the investigation, as this may interfere with the ongoing LE inquiry and

violate the FI’s policies and procedures. The investigator should also not contact local LE directly, as

this may compromise the confidentiality of the investigation and the FIU’s authority. Reference:

Advanced CAMS-FCI Study Guide, Chapter 4: Reporting Suspicious Activity, pages 40-411

Advanced CAMS-FCI Study Guide, Chapter 5: Governance of an AFC Investigations Unit, pages 48-491

Advanced CAMS-FCI Certification | ACAMS

Question 2

The investigative department of a financial institution (Fl) receives an internal escalation notice from

the remittance department for a SWIFT message requesting a refund due to potential fraud. The

notice indicates that a total of three international incoming remittances were transferred to a

corporate customer from Country A, in the amount of approximately 5 million EUR for each. The first

two incoming remittances had been exchanged into currency B and transferred out to Country B a

few days ago. The third incoming remittance has been held by the remittance department.

As noted from the KYC profile, the corporate customer is working in the wood industry. with the last

account review completed 3 months ago. Since the account's opening. there has been no history of a

large amount of funds flowing through the account. The investigator conducts an Internet search and

finds that the remitter is a food beverage company.

The same morning, the investigator receives a call from a financial intelligence unit (FIU) inquiring

about the same incident. The FIU states that it will issue a warrant to freeze the account on the same

day.

Which steps for documenting the final investigation decision are appropriate for the investigator in

this scenario?

- A. Exclude any open-source information from record-keeping since it is publicly available.

- B. Add all of the information the Fl has about the subject, their account(s) activity, research results. KYC information, etc. to the SAR/STR.

- C. Document the investigation process and retain all relevant documents in the case management system.

- D. Do not document the investigation process if a SAR/STR is not filed.

Answer:

C

Explanation:

The investigator should document the investigation process and retain all relevant documents in the

case management system. This is because documenting the investigation process is a good practice

to ensure the quality and consistency of the investigation, as well as to facilitate the review and audit

of the investigation. Retaining all relevant documents is also important to support the evidence and

findings of the investigation, as well as to comply with the record-keeping requirements of the

relevant authorities. The other options are incorrect because:

A . Excluding any open-source information from record-keeping is not advisable, as open-source

information can provide valuable insights and context for the investigation, and may not be easily

retrievable in the future.

B . Adding all of the information the FI has about the subject, their account(s) activity, research

results, KYC information, etc. to the SAR/STR is not necessary, as the SAR/STR should only contain the

essential information that is relevant and material to the suspicious activity. Adding too much

information may obscure the main points and make the SAR/STR less effective.

D . Not documenting the investigation process if a SAR/STR is not filed is not acceptable, as the

investigation process should be documented regardless of the outcome. Documenting the

investigation process can help justify why a SAR/STR was not filed, and also provide a reference for

future investigations involving the same subject or activity.

Reference:

Advanced CAMS-FCI Certification | ACAMS

, Section 3: Reporting Suspicious Activity, page 14

Leading Complex Investigations Certificate | ACAMS

, Module 4: Documenting Your Investigation,

page 4

Question 3

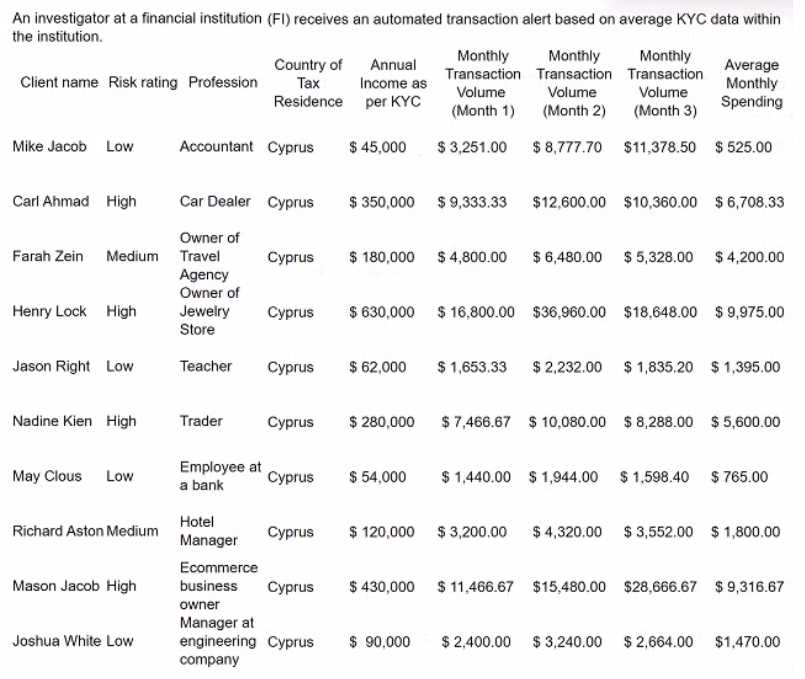

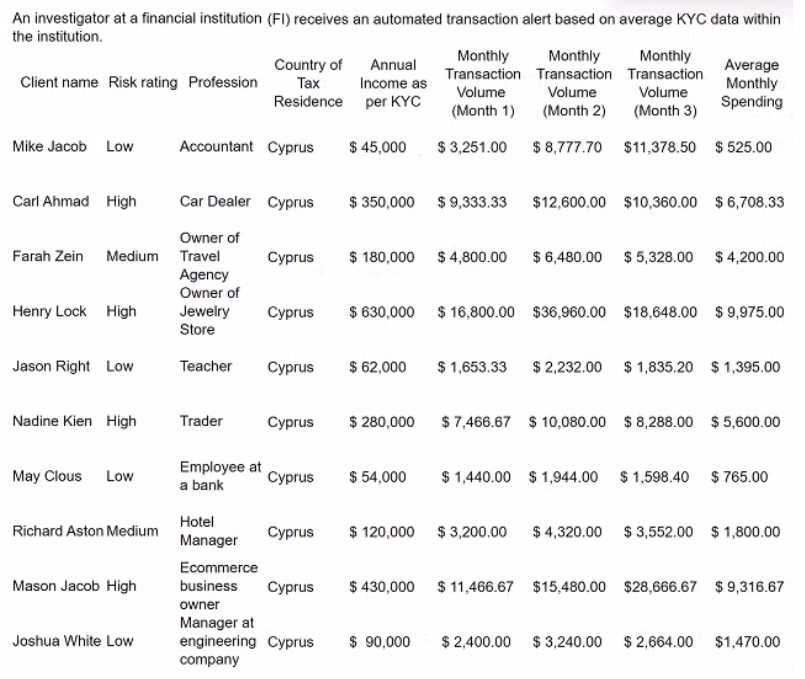

Refer to the exhibit.

In a review of the account activity associated with Nadine Kien, an investigator observes a large

number of small- to medium-size deposits from numerous individuals from several different global

regions. The money is then transferred to a numbered company. Which is the next best course of

action for the investigator?

- A. Complete the monthly review and note the activity for next month's review.

- B. File a SAR/STR on the account activity in relation to a potential funnel account.

- C. Recommend the account for exit due to frequent global transactions.

- D. No further action is required as the customer is already rated at high-risk and the monthly spending is within expectations.

Answer:

B

Explanation:

The next best course of action for the investigator is to file a SAR/STR on the account activity in

relation to a potential funnel account. This is because a funnel account is a type of money laundering

scheme that involves depositing funds from multiple sources into a single account, and then

transferring them to another account, often in a different jurisdiction. A funnel account can be used

to conceal the origin, ownership, and destination of illicit funds, and to evade currency transaction

reporting requirements. The investigator should report the suspicious activity to the relevant

authorities and document the findings and actions taken. The other options are incorrect because:

A . Completing the monthly review and noting the activity for next month’s review is not sufficient,

as it delays the reporting of a possible money laundering scheme and exposes the financial

institution to regulatory and reputational risks.

C . Recommending the account for exit due to frequent global transactions is not appropriate, as it

does not address the underlying issue of potential money laundering and may alert the customer of

the investigation.

D . No further action is required as the customer is already rated at high-risk and the monthly

spending is within expectations is not acceptable, as it ignores the red flags of a funnel account and

fails to comply with the anti-money laundering obligations of the financial institution.

Reference:

Advanced CAMS-FCI Certification | ACAMS, Section 2: Investigating Financial Crimes, page 9

Leading Complex Investigations Certificate | ACAMS, Module 2: Identifying Red Flags, page 5

Question 4

Refer to the exhibit.

During a review of the accounts related to Richard Aston, an investigator notices a high number of

incoming payments from various individuals. They also notice that these incoming payments

typically occur during large sporting events or conferences. As a result of the account review, of

which illegal activity does the investigator have reasonable grounds to suspect Richard Aston?

- A. Embezzling from the hotel

- B. Aftermarket sales of entertainment admission tickets

- C. Human trafficking

- D. Sports betting

Answer:

B

Explanation:

The illegal activity that the investigator has reasonable grounds to suspect Richard Aston of is

aftermarket sales of entertainment admission tickets. This is because aftermarket sales of

entertainment admission tickets involve reselling tickets for events, concerts, festivals, etc. at a

higher price than their face value, often through online platforms or scalpers. This practice can be

illegal or unethical, depending on the jurisdiction and the terms and conditions of the original ticket

seller. The investigator should look for indicators of aftermarket sales of entertainment admission

tickets, such as high volume or frequency of incoming payments from various individuals, correlation

between incoming payments and major events or conferences, and discrepancy between the

customer’s profile and the nature of the transactions. The other options are incorrect because:

A . Embezzling from the hotel is not likely, as it would involve stealing money or property from the

hotel by an employee or a person in a position of trust. There is no evidence that Richard Aston

works for or has access to the hotel’s assets.

C . Human trafficking is not probable, as it would involve exploiting people for forced labor or

commercial sexual exploitation. There is no indication that Richard Aston is involved in any form of

human trafficking or has any connection to victims or perpetrators.

D . Sports betting is not plausible, as it would involve wagering money on the outcome of sporting

events or games. There is no sign that Richard Aston is engaged in any sports betting activity or has

any association with bookmakers or gamblers.

Reference:

Advanced CAMS-FCI Certification | ACAMS, Section 2: Investigating Financial Crimes, page 10

TicketSwap: The safest way to buy and sell tickets

Ticketing 101 | Ticketmaster

10 Types of Tickets For Events (+ Why & When To Use Them) - Eventbrite

Question 5

An investigator is reviewing an alert for unusual activity. System scanning detected a text string

within a company customer's account transactions that indicates the account may have been used

for a drug or drug paraphernalia purchase Based on the KYC profile, the investigator determines the

customer's company name and business type are marketed as a gardening supplies company. The

investigator reviews the account activity and notes an online purchase transaction that leads the

investigator to a website that sells various strains of marijuan

a. Additional account review detects cash deposits into the account at the branch teller lines, so the

investigator reaches out to the teller staff regarding the transactions. The teller staff member reports

that the business customers have frequently deposited cash in lower amounts. The teller, without

prompting, adds that one of the transactors would occasionally smell of a distinct scent of marijuana

smoke.

Which are the best next steps for the investigator to take? (Select Three.)

- A. Review the customer's transaction history.

- B. Request information from the internet service provider who hosts the website.

- C. Check internal KYC information.

- D. Research other customer accounts for transactions to the same website.

- E. Conduct adverse media and open-source searches on the customer's background.

- F. Identify if the customer has opened accounts in an urban city area.

Answer:

A, C, E

Explanation:

The best next steps for the investigator to take are:

A . Review the customer’s transaction history. This can help the investigator identify any patterns or

anomalies in the customer’s account activity, such as changes in transaction volume, frequency,

amount, source, destination, purpose, etc. The investigator can also compare the customer’s

transaction history with their KYC profile and risk rating to assess if there are any discrepancies or

inconsistencies.

C . Check internal KYC information. This can help the investigator verify the customer’s identity,

business nature, ownership structure, expected activity, source of funds, etc. The investigator can

also update or enhance the customer’s KYC information based on any new or relevant information

obtained from other sources.

E Conduct adverse media and open-source searches on the customer’s background. This can help the

investigator find out if there is any negative or adverse information about the customer in public data

sources, such as news articles, social media posts, blogs, forums, etc. Adverse media and open-

source searches can also provide additional context and insight into the customer’s reputation,

behavior, associations, etc. The other options are incorrect because:

B . Request information from the internet service provider who hosts the website is not feasible, as it

may require a legal process or a court order to obtain such information. Moreover, the internet

service provider may not have or disclose any useful information about the website or its owner.

D . Research other customer accounts for transactions to the same website is not relevant, as it may

not provide any meaningful information about the customer under investigation. Furthermore, it

may violate the privacy and confidentiality of other customers who are not related to the

investigation.

F . Identify if the customer has opened accounts in an urban city area is not helpful, as it may not

have any bearing on the customer’s involvement in a drug or drug paraphernalia purchase.

Additionally, it may not be possible to access or verify such information without the customer’s

consent or authorization.

Reference:

Advanced CAMS-FCI Certification | ACAMS, Section 2: Investigating Financial Crimes, page 11

Leading Complex Investigations Certificate | ACAMS, Module 3: Conducting Research and Analysis,

page 6

Adverse Media Screening - Using AI to Mitigate Risk

Legal requirements for adverse media screening - Thomson Reuters

Electronic client due diligence | Ethics helpsheets | ICAEW

6AMLD & FATF: Where Adverse Media Screening Fits In

Free Adverse Media Check | NameScan

Question 6

An investigator is reviewing an alert for unusual activity. System scanning detected a text string

within a company customer's account transactions that indicates the account may have been used

for a drug or drug paraphernalia purchase. Based on the KYC profile, the investigator determines the

customer's company name and business type are marketed as a gardening supplies company. The

investigator reviews the account activity and notes an online purchase transaction that leads the

investigator to a website that sells various strains of marijuan

a. Additional account review detects cash deposits into the account at the branch teller lines, so the

investigator reaches out to the teller staff regarding the transactions. The teller staff member reports

that the business customers have frequently deposited cash in lower amounts. The teller, without

prompting, adds that one of the transactors would occasionally smell of a distinct scent of marijuana

smoke.

Which information should be included in the SAR/STR?

- A. The customer information, including KYC background

- B. A transaction that is commensurate with the customer's background

- C. The fact that one of the transactors occasionally smelled of marijuana smoke

- D. Details of the transactor's social media accounts

Answer:

C

Explanation:

The SAR/STR should include any information that is relevant to the suspicious activity, such as the

customer information, the transaction details, and any other indicators of potential money

laundering or criminal activity. The fact that one of the transactors occasionally smelled of marijuana

smoke is an indicator that the customer may be involved in the illicit drug trade, which is a predicate

offense for money laundering. Therefore, this information should be included in the SAR/STR.

Reference: Advanced CAMS-FCI Study Guide, page 25.

Question 7

A financial institution (Fl) banks a money transmitter business (MTB) located in Miami. The MTB

regularly initiates wire transfers with the ultimate beneficiary in Cuba and legally sells travel

packages to Cub

a. The wire transfers for money remittances comply with the country's economic sanctions policies. A

Fl investigator on the sanctions team reviews each wire transfer to ensure compliance with sanctions

and to monitor transfer details.

An airline located in Cuba, unrelated to the business, legally sells airline tickets in Cuba to Cuban

citizens wanting to travel outside of Cuba. The airline tickets are purchased using Cuban currency

(CUC).

The MTB wants 100,000 USD worth of CUC. Purchasing CUC from a Cuban bank includes a 4% fee.

The MTB contacts the airline to ask if the airline will trade its CUC for USD at a lower exchange fee

than the Cuban bank. The airline agrees to a 1% fee. The MTB initiates a wire transfer to the airline

which appears as normal activity in the monitoring system because of the business' travel package

sales.

Which investigative actions should the investigator take concerning the 100.000 USD wire transfer?

(Select Three.)

- A. Review the wire transfer protocols for this customer.

- B. Gather all account activity for Fl clients that purchased packages from the airline.

- C. Review a sampling of wire transfers initiated by travel companies with Cuba travel packages.

- D. Recommend a plan for the Fl's management to restrict the account relationship.

- E. Review regulations applicable to foreign currency trading transactions.

- F. Locate and review licenses, registrations, and account operating agreements associated with the MTB account.

Answer:

A, E, F

Explanation:

The investigator should take the following investigative actions concerning the 100,000 USD wire

transfer:

Review the wire transfer protocols for this customer. This will help the investigator to determine if

the wire transfer is consistent with the customer’s normal business activity and risk profile, or if it

deviates from the established patterns or thresholds.

Review regulations applicable to foreign currency trading transactions. This will help the investigator

to assess if the wire transfer violates any laws or regulations related to currency exchange, such as

reporting requirements, licensing requirements, or sanctions compliance.

Locate and review licenses, registrations, and account operating agreements associated with the

MTB account. This will help the investigator to verify if the MTB has the necessary authorization and

documentation to conduct currency exchange transactions and if it has disclosed this activity to the

FI. Reference: Advanced CAMS-FCI Study Guide, pages 32-33.

Question 8

A financial institution (Fl) banks a money transmitter business (MTB) located in Miami. The MTB

regularly initiates wire transfers with the ultimate beneficiary in Cuba and legally sells travel

packages to Cub

a. The wire transfers for money remittances comply with the country's economic sanctions policies. A

Fl investigator on the sanctions team reviews each wire transfer to ensure compliance with sanctions

and to monitor transfer details.

An airline located in Cuba, unrelated to the business, legally sells airline tickets in Cuba to Cuban

citizens wanting to travel outside of Cuba. The airline tickets are purchased using Cuban currency

(CUC).

The MTB wants 100,000 USD worth of CUC. Purchasing CUC from a Cuban bank includes a 4% fee.

The MTB contacts the airline to ask if the airline will trade its CUC for USD at a lower exchange fee

than the Cuban bank. The airline agrees to a 1% fee. The MTB initiates a wire transfer to the airline

which appears as normal activity in the monitoring system because of the business' travel package

sales.

The investigator recommends that a SAR/STR be filed. What documentation should be referenced in

the SAR/STR filing? (Select Three.)

- A. All documents related to the agreement between the airline and the MTB

- B. Cumulative dollar amount of the wire transfer activity

- C. Airline's ticket sales and passenger list

- D. Cumulative dollar amount for transactions listing for all the MTB account's wire activity regarding travel packages

- E. Licensing information regarding the travel agency providing tourist sales to Cuba

- F. Account documentation on all related accounts maintained by the MTB

Answer:

B

Explanation:

The most likely reason for conducting a reverse transaction is to conceal or launder illicit funds. A

reverse transaction is a transaction that reverses a previous transaction, such as a refund, a

chargeback, or a cancellation. Reverse transactions can be used by money launderers to obscure the

source, ownership, or destination of funds, or to create false records or invoices. For example, a

money launderer may initiate a wire transfer from a high-risk jurisdiction to a low-risk jurisdiction,

and then reverse the transaction after receiving confirmation of the funds. This way, the money

launderer can create a paper trail that shows legitimate funds coming from a low-risk jurisdiction,

while hiding the true origin of the funds.

Reference: Advanced CAMS-FCI Study Guide, page 40-41.

Question 9

An investigator at a corporate bank is conducting transaction monitoring alerts clearance.

KYC profile background: An entity customer, doing business offshore in Hong Kong, established a

banking business relationship with the bank in 2017 for deposit and loan purposes. It acts as an

offshore investment holding company. The customer declared that the ongoing source of funds to

this account comes from group-related companies.

• X is the UBO. and owns 97% shares of this entity customer;

• Y is the authorized signatory of this entity customer. This entity customer was previously the

subject of a SAR/STR.

KYC PROFILE

Customer Name: AAA International Company. Ltd

Customer ID: 123456

Account Opened: June 2017

Last KYC review date: 15 Nov 2020

Country and Year of Incorporation: The British Virgin Islands, May 2017

AML risk level: High

Account opening and purpose: Deposits, Loans and Trade Finance

Anticipated account activities: 1 to 5 transactions per year and around 1 million per

transaction amount

During the investigation, the investigator reviewed remittance transactions activities for the period

from Jul 2019 to Sep 2021 and noted the following transactions pattern:

TRANSACTION JOURNAL

Review dates: from July 2019 to Sept 2021

For Hong Kong Dollars (HKD) currency:

Incoming transactions: 2 inward remittances of around 1.88 million HKD in total from

different third parties

Outgoing transactions: 24 outward remittances of around 9 4 million HKD in total to

different third parties

For United States Dollars (USD) currency:

Incoming transactions: 13 inward remittances of around 3.3 million USD in total from

different third parties

Outgoing transactions: 10 outward remittances of around 9.4 million USD in total to

different third parties.

RFI Information and Supporting documents:

According to the RFI reply received on 26 May 2021, the customer provided the bank

with the information below:

1) All incoming funds received in HKD & USD currencies were monies lent from non-customers of the

bank. Copies of loan agreements had been provided as supporting documents. All of the loan

agreements were in the same format and all the lenders are engaged in trading business.

2) Some loan agreements were signed among four parties, including among lenders. borrower (the

bank's customer), guarantor, and guardian with supplemental agreements, which stated that the

customer, as a borrower, who failed to repay the loan

Based on the KYC profile and the transaction journal, the pattern of activity shows a deviation in:

- A. expected vs. actual activity.

- B. customer risk rating

- C. product risk rating.

- D. U.S. currency incoming vs. outgoing transaction rales.

Answer:

A

Explanation:

The correct answer is A because the expected account activities were 1 to 5 transactions per year and

around 1 million per transaction amount, but the actual activity showed much more frequent and

varied transactions in different currencies and amounts. This indicates a deviation from the

customer’s profile and risk level.

Reference: Advanced CAMS-FCI Study Guide, page 16

Question 10

An investigator at a corporate bank is conducting transaction monitoring alerts clearance.

KYC profile background: An entity customer, doing business offshore in Hong Kong, established a

banking business relationship with the bank since 2017 for deposit and loan purposes. It acts as an

offshore investment holding company. The customer declared that the ongoing source of funds to

this account comes from group-related companies.

• X is the UBO. and owns 97% shares of this entity customer;

• Y is is the authorized signatory of this entity customer. This entity customer was previously the

subject of a SAR/STR.

KYC PROFILE

Customer Name: AAA International Company. Ltd

Customer ID: 123456

Account Opened: June 2017

Last KYC review date: 15 Nov 2020

Country and Year of Incorporation: The British Virgin Islands, May 2017

AML risk level: High

Account opening and purpose: Deposits, Loans, and Trade Finance

Anticipated account activities: 1 to 5 transactions per year and around 1 million per

transaction amount

During the investigation, the investigator reviewed remittance transactions activities for the period

from Jul 2019 to Sep 2021 and noted the following transactions pattern:

TRANSACTION JOURNAL

Review dates: from July 2019 to Sept 2021

For Hong Kong Dollars (HKD) currency:

Incoming transactions: 2 inward remittances of around 1.88 million HKD in total from

different third parties

Outgoing transactions: 24 outward remittances of around 9 4 million HKD in total to

different third parties

For United States Dollars (USD) currency:

Incoming transactions: 13 inward remittances of around 3.3 million USD in total from

different third parties

Outgoing transactions: 10 outward remittances of around 9.4 million USD in total to

different third parties.

RFI Information and Supporting documents:

According to the RFI reply received on 26 May 2021, the customer provided the bank

with the information below:

1J All incoming funds received in HKD & USD currencies were monies lent from non-customers of the

bank. Copies of loan agreements had been provided as supporting documents. All of the loan

agreements were in the same format and all the lenders are engaged in trading business.

2) Some loan agreements were signed among four parties, including among lenders. borrower (the

bank's customer), guarantor, and guardian with supplemental agreements, which stated that the

customer, as a borrower, who failed to repay a loan

Which suspicious activity should the investigator identify during the review of the loan agreements?

- A. AAA International Company Ltd.'s account has transactions in HKD and USD.

- B. Y is the authorized signatory on the beneficial ownership form.

- C. Online information found that X is the chairman of a business group of companies.

- D. Y signed on behalf of the lenders.

Answer:

D

Explanation:

The correct answer is D because it is a suspicious activity that Y, who is the authorized signatory of

the customer, also signed on behalf of the lenders. This indicates a possible conflict of interest,

collusion, or fraud. The other options are not suspicious activities based on the information given.

Reference: [Advanced CAMS-FCI Study Guide], page 17-18

Question 11

An investigator at a corporate bank is conducting transaction monitoring alerts clearance.

KYC profile background: An entity customer, doing business offshore in Hong Kong, established a

banking business relationship with the bank in 2017 for deposit and loan purposes. It acts as an

offshore investment holding company. The customer declared that the ongoing source of funds to

this account comes from group-related companies.

• X is the UBO. and owns 97% shares of this entity customer;

• Y is the authorized signatory of this entity customer. This entity customer was previously the

subject of a SAR/STR.

KYC PROFILE

Customer Name: AAA International Company. Ltd

Customer ID: 123456

Account Opened: June 2017

Last KYC review date: 15 Nov 2020

Country and Year of Incorporation: The British Virgin Islands, May 2017

AML risk level: High

Account opening and purpose: Deposits, Loans, and Trade Finance

Anticipated account activities: 1 to 5 transactions per year and around 1 million per

transaction amount

During the investigation, the investigator reviewed remittance transactions activities for the period

from Jul 2019 to Sep 2021 and noted the following transactions pattern:

TRANSACTION JOURNAL

Review dates: from July 2019 to Sept 2021

For Hong Kong Dollars (HKD) currency:

Incoming transactions: 2 inward remittances of around 1.88 million HKD in total from

different third parties

Outgoing transactions: 24 outward remittances of around 9 4 million HKD in total to

different third parties

For United States Dollars (USD) currency:

Incoming transactions: 13 inward remittances of around 3.3 million USD in total from

different third parties

Outgoing transactions: 10 outward remittances of around 9.4 million USD in total to

different third parties.

RFI Information and Supporting documents:

According to the RFI reply received on 26 May 2021, the customer provided the bank

with the information below:

1J All incoming funds received in HKD & USD currencies were monies lent from non-customers of the

bank. Copies of loan agreements had been provided as supporting documents. All of the loan

agreements were in the same format and all the lenders are engaged in trading business.

2) Some loan agreements were signed among four parties, including among lenders. borrower (the

bank's customer), guarantor, and guardian with supplemental agreements, which stated that the

customer, as a borrower, who failed to repay the loan

Which additional information would support escalating this account for closure?

- A. The bank files SARs/STRs indicating that Y opened accounts for small companies located in close proximity to the bank.

- B. A follow-up request reveals that the account receives funds from loans, collects payments from group-related companies, and sends the payments to the lenders.

- C. A review of outward remittances reveals the same pattern of several simple steps for each transaction,

- D. A review of X's personal bank account shows that X received wire transfers that aggregate the amounts transferred to the group-related companies.

Answer:

C

Explanation:

A review of outward remittances reveals the same pattern of several simple steps for each

transaction, which could indicate a layering scheme to obscure the origin and destination of the

funds. This would support escalating this account for closure, as it is inconsistent with the customer’s

declared purpose and anticipated activities. The other options are not relevant or sufficient to

warrant account closure.

Reference: Advanced CAMS-FCI Certification | ACAMS

Question 12

An investigator at a corporate bank is conducting transaction monitoring alerts clearance.

KYC profile background: An entity customer, doing business offshore in Hong Kong, established a

banking business relationship with the bank since 2017 for deposit and loan purposes. It acts as an

offshore investment holding company. The customer declared that the ongoing source of funds to

this account comes from group-related companies.

• X is the UBO. and owns 97% shares of this entity customer;

• Y is is the authorized signatory of this entity customer. This entity customer was previously the

subject of a SAR/STR.

KYC PROFILE

Customer Name: AAA International Company. Ltd

Customer ID: 123456

Account Opened: June 2017

Last KYC review date: 15 Nov 2020

Country and Year of Incorporation: The British Virgin Islands, May 2017

AML risk level: High

Account opening and purpose: Deposits, Loans and Trade Finance

Anticipated account activities: 1 to 5 transactions per year and around 1 million per

transaction amount

During the investigation, the investigator reviewed remittance transactions activities for the period

from Jul 2019 to Sep 2021 and noted the following transactions pattern:

TRANSACTION JOURNAL

Review dates: from July 2019 to Sept 2021

For Hong Kong Dollars (HKD) currency:

Incoming transactions: 2 inward remittances of around 1.88 million HKD in total from

different third parties

Outgoing transactions: 24 outward remittances of around 9 4 million HKD in total to

different third parties

For United States Dollars (USD) currency:

Incoming transactions: 13 inward remittances of around 3.3 million USD in total from

different third parties

Outgoing transactions: 10 outward remittances of around 9.4 million USD in total to

different third parties.

RFI Information and Supporting documents:

According to the RFI reply received on 26 May 2021, the customer provided the bank

with the information below:

1) All incoming funds received in HKD & USD currencies were monies lent from non-customers of the

bank. Copies of loan agreements had been provided as supporting documents. All of the loan

agreements were in the same format and all the lenders are engaged in trading business.

2) Some loan agreements were signed among four parties, including among lenders. borrower (the

bank's customer), guarantor, and guardian with supplemental agreements, which stated that the

customer, as a borrower, who failed to repay the loan

After reviewing the transaction journal, request for information response, and supporting

documentation, the investigator determines that additional information is needed. Which additional

information should the investigator request?

- A. Previously filed SARVSTR unrelated to the customer, but similar in content

- B. Formation document/description of the group-related companies

- C. Source of the incoming funds to the group-related companies

- D. Adverse news screening on all names listed in the formation documents

Answer:

C

Explanation:

The additional information that the investigator should request is the source of the incoming funds to

the group-related companies. This is because the customer declared that the ongoing source of

funds to this account comes from group-related companies, but the transaction journal shows that

the customer received funds from different third parties, not from group-related companies.

Therefore, the investigator should verify the relationship and legitimacy of these third parties and

their funds with the customer and the group-related companies. The other options are not relevant

or necessary for this investigation.

Reference: Advanced CAMS-FCI Certification | ACAMS

Question 13

CLIENT INFORMATION FORM Client Name: ABC Tech Corp Client ID. Number: 08125 Name: ABC Tech

Corp Registered Address: Mumbai, India Work Address: Mumbai, India Cell Phone: "*•"'" Alt Phone:

"*""* Email: ........"

Client Profile Information:

Sector: Financial

Engaged in business from (date): 02 Jan 2020 Sub-sector: Software-Cryptocurrency Exchange

Expected Annual Transaction Amount: 125,000 USD Payment Nature: Transfer received from clients’

fund

Received from: Clients

Received for: Sale of digital assets

The client identified itself as Xryptocurrency Exchange." The client has submitted the limited liability

partnership deed. However, the bank's auditing team is unable to identify the client's exact business

profile as the cryptocurrency exchange specified by the client as their major business awaits

clearance from the country's regulator. The client has submitted documents/communications

exchanged with the regulator and has cited the lack of governing laws in the country of their

operation as the reason for the delay.

During the financial crime investigation, the investigator discovers that some of the customer due

diligence (CDD) documents submitted by the client were fraudulent. The investigator also finds that

some of the information in the financial institution's information depository is false. What should the

financial crime investigator do next?

- A. Report collusion between the cryptocurrency exchange and internal staff in the internal hotline or whistle-blowing channel.

- B. Request that the relationship manager conduct a CDD refresh as it is a material trigger.

- C. Escalate to the compliance officer/money laundering reporting officer to file a SAR/STR.

- D. Contact the client directly and obtain the relevant notarized documents and information.

Answer:

C

Explanation:

The correct answer is C. Escalate to the compliance officer/money laundering reporting officer to file

a SAR/STR. This is because the financial crime investigator has found evidence of fraudulent

documents and false information, which indicate a high risk of money laundering or other financial

crimes. The investigator should not contact the client directly, as this may tip them off or

compromise the investigation. The investigator should also not report collusion between the

cryptocurrency exchange and internal staff, as this is an assumption that has not been verified. The

investigator should not request a CDD refresh, as this is not sufficient to address the serious issues

identified.

Reference:

Advanced CAMS-FCI Study Guide, page 291

Advanced CAMS-FCI Study Guide, page 311

Advanced CAMS-FCI Study Guide, page 331

1:

https://www.acams.org/en/certifications/advanced-cams/advanced-financial-crimes-

investigations

Question 14

CLIENT INFORMATION FORM Client Name: ABC Tech Corp Client I.D. Number: 08125 Name: ABC

Tech Corp Registered Address: Mumbai, India Work Address: Mumbai. India Cell Phone: *

■

*•"— Alt

Phone: Email: *•*•*«•*•

Client Profile Information:

Sector: Financial

Engaged in business from (date): 02 Jan 2020

Sub-sector: Software-Cryptocurrency Exchange

Expected Annual Transaction Amount: 125.000 USD

Payment Nature: Transfer received from client’s fund

Received from: Clients

Received for: Sale of digital assets

The client identified themselves as "Cryptocurrency Exchange" Client has submitted the limited

liability partnership deed. However, the bank's auditing team is unable to identify the client's exact

business profile as the cryptocurrency exchange specified by the client as their major business awaits

clearance from the country's regulator. The client has submitted documents/communications

exchanged with the regulator and has cited the lack of governing laws in the country of their

operation as the reason for the delay.

Investigators determine the ultimate beneficial owner of ABC Tech Corp is a high-net-worth client.

The client owns a real estate agency left to her when her spouse died. The spouse provided seed

capital for ABC Tech Corp through a direct 1,000.000 Great British Pound (GBP) deposit.

What additional information would trigger filing a SAR/STR?

- A. The client's spouse's source of wealth was a salary of 250,000 GBP per annum for the past 4 years and rental of properties of 150,000 GBP per annum for the past 6 years.

- B. The client's current net asset value is 8 million GBP, of which 7.5 million GBP was derived from the inheritance.

- C. An open-source search revealed that the client's spouse was a PEP.

- D. The funds for the seed capital were in the form of 50 cashier's checks of 10,000 GBP each and 50 money orders of 10,000 GBP.

Answer:

D

Explanation:

The additional information that would trigger filing a SAR/STR is the fact that the funds for the seed

capital were in the form of 50 cashier’s checks of 10,000 GBP each and 50 money orders of 10,000

GBP. This is because this indicates a possible attempt to avoid the reporting threshold of 10,000 GBP

for cash transactions, which is a common money laundering technique known as structuring or

smurfing12. The other options are not necessarily suspicious, as they do not involve cash

transactions or indicate any illicit source of funds. The fact that the client’s spouse was a PEP does

not automatically make the transaction suspicious unless there are other red flags or risk factors

associated with the PEP34

Reference: 1: Money Laundering Techniques 2: Structuring 3: Politically exposed person 4: PEP

Definition & Meaning - Merriam-Webster

Question 15

During transaction monitoring. Bank A learns that one of their customers. Med Supplies 123. is

attempting to make a payment via wire totaling 382,500 USD to PPE Business LLC located in Mexico

to purchase a large order of personal protective equipment. specifically surgical masks and face

shields. Upon further verification. Bank A decides to escalate and refers the case to investigators.

Bank A notes that, days prior to the above transaction, the same customer went to a Bank A location

to wire 1,215,280 USD to Breath Well LTD located in Singapore. Breath Well was acting as an

intermediary to purchase both 3-ply surgical masks and face shields from Chin

a. Bank A decided not to complete the transaction due to concerns with the involved supplier in

China. Moreover, the customer is attempting to send a third wire in the amount of 350,000 USD for

the purchase of these items, this time using a different vendor in China. The investigator must

determine next steps in the investigation and what actions, if any. should be taken against relevant

parties.

During the investigation, Bank A receives a USA PATRIOT Act Section 314(a) request related to Med

Supplies 123. Which steps should the investigator take when fulfilling the request? (Select Three.)

- A. Exit the relationship with the business since it appears that customer is under investigation.

- B. Do not respond to Financial Crimes Enforcement Network (FinCEN) if the requested information is not present in the financial institution's system of records.

- C. Review the account(s) activity and proactively file a SAR/STR using the 314(a) request as the basis for the filing.

- D. Report to Financial Crimes Enforcement Network (FinCEN) that a match was found without revealing any other details.

- E. Report back to the Financial Crimes Enforcement Network (FinCEN) within 15 days of receipt of the request via a secure internet website.

- F. Search its records expeditiously to determine whether it maintains(ed) any accounts for the subject(s) listed in the request.

Answer:

D, E, F

Explanation:

According to the FinCEN’s 314(a) Fact Sheet1, the steps that the investigator should take when

fulfilling the request are:

Search its records expeditiously to determine whether it maintains(ed) any accounts for the

subject(s) listed in the request. This is option F.

Report back to the Financial Crimes Enforcement Network (FinCEN) within 15 days of receipt of the

request via a secure internet website. This is option E.

Report to Financial Crimes Enforcement Network (FinCEN) that a match was found without revealing

any other details. This is option D.

The other options are incorrect because:

Exiting the relationship with the business since it appears that customer is under investigation is not

required by the 314(a) program and may interfere with law enforcement’s investigation. This is

option A.

Not responding to Financial Crimes Enforcement Network (FinCEN) if the requested information is

not present in the financial institution’s system of records is contrary to the 314(a) program, which

requires financial institutions to respond whether or not they have a match. This is option B.

Reviewing the account(s) activity and proactively filing a SAR/STR using the 314(a) request as the

basis for the filing is not appropriate, as the 314(a) request itself is not a sufficient reason to file a

SAR/STR. The financial institution should only file a SAR/STR if it has its own independent suspicion

of money laundering or terrorist financing. This is option C.

Reference: 1: FinCEN’s 314(a) Fact Sheet